This is similar to “shares authorized,” the maximum number of shares a company is allowed to issue. The credit limit on a card does not mean you have to charge $5,000 on your first purchase but instead that you may continue to charge purchases up until you have reached a $5,000 maximum. Smaller numbers of shares may be sold over time up to the maximum of the number of shares authorized. Occasionally, a corporation will buy back its own shares on the open market.

Financial Accounting

Rather, the dividends on common stock are generally announced as a certain dollar amount per share, like $5 per share or $10 per share, etc. To determine the dividend yield metric, investors can simply divide this per share dividend amount by the per share cost. Stock issuance is when a company sells new shares to investors.

Common Stock Issued for Non-Cash Exchange

For example, the company ABC issues 20,000 shares of common stock at par value for cash. Common shares are one type of security that companies may issue to raise capital. The most mysterious term on a set of financial statements might well be “par value.” The requirement for a par value to be set was created decades ago in connection with the issuance of stock.

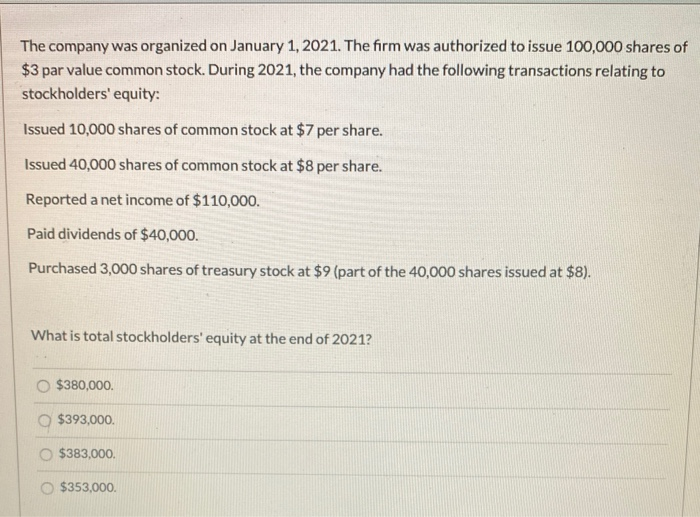

Issuance of common stock journal entry

But no one shareholder allowed an allocation of more than one bundle. So we now have to prepare two journal entries – which we’ll combine into one. The first is the allotment of the shares, and the second is to return the monies to those not awarded any shares.

4: Issuing Stock for Non-Cash Assets

Therefore, the journal entries for this process will be as follows. The debit to the share capital account removes the 100,000 class A shares from ABC’s equity. The $1,400,000 debit to the additional paid-in capital account also reduces ABC’s equity section.

- For instance, some businesses will issue stock in exchange for tangible assets or real property.

- Moreover, the company may issue a share to acquire another company by giving the business owner share equity.

- If the company issues only one type of stock, it is common stock.

- Watch this video to demonstrate par and no-par value transactions.

- The market price per share, on the other hand, refers to the per share value or worth at which a company’s stock is actually traded in the secondary market.

- The prospectus stated that on allotment of shares, the shareholder would have 30 days to deposit the required 50 per cent of the share price.

Resale the Treasury Stock (stock buyback)

As mentioned, nowadays, par value has nothing to do with the market value of the common stock and it is just a number on the paper. Likewise, investors typically do not deem that the par value of the common stock is necessary to exist before they purchase the stock for their investments. It is useful to note that in many jurisdictions, issuing the common stock below par value is not allowed and is considered illegal. Additionally, even though some jurisdictions allow the issuance of the common stock below its par value, such activity is usually very rare. At the time of the formation of the corporation, the market value of our common stock cannot be determined yet.

During negotiations, officials for Maine offer to issue ten thousand shares of $1 par value common stock for this property. The shares are currently selling on a stock exchange for $12 each. The investor decides to accept this proposal rather than go to the trouble of trying to sell the land. On the other hand, if the stock price equal to the par value, only cash and common stock on the balance sheet will be affected as the result of the issuance of the stock.

After Board approval, ABC’s accounts team would prepare the following journal entry. We have now reached December, and the second and final call for class A shares is now coming due. We would repeat the journal entries we created for the first call. So for completeness of the example, the following journal entries would be made by ABC’s accounts team. The debit to the bank account reflects the $400,000 ABC now has from its first call on the class A shares. And the credit to the call account can now be closed as this money is no longer due from shareholders.

The cost method of accounting for common stock buy-backs is the simplest approach and caters well for the three scenarios you might face. We’ll look at each scenario providing the journal entries and calculations required. The prospectus irs overhauls form w stated that on allotment of shares, the shareholder would have 30 days to deposit the required 50 per cent of the share price. So over August, we would see the entry below prepared by ABC Ltd each time allotment money is received.

The credit entry to the Class A Share Application reflects the liability the company also holds. And as we’ll see, some people will be getting their money back. Common stock forms part of the equity section of a company – or sometimes referred to as the capital of a company. Therefore you will find common stock disclosed in the balance sheet (often referred to as the statement of financial position). Of course, the par value of the common stock has nothing to do with its market value. And the real value of how much a company’s shares are actually worth and sold for is the market value, not the par value.